Looking at Lancashire

What does the data say about the last part of the North to get a mayor?

This is the last in a series about the Northern Economy, looking at the economic data for all eleven parts of the North. I’ve left Lancashire until last, not because the area stretching from Blackpool to Burnley isn’t interesting - but mainly because despite already having a Combined Authority - it hasn’t got a mayor yet and looks set to be the last part of the North to eventually go down that route. This is something I’ll come back to later.

Looking at the leaderboard of Northern productivity, Lancashire comes out in the middle of the pack, though above the UK average, for the period 2019 to 2023. As we know, productivity is probably the most important statistic for understanding an economy as it tells us how much value is being created for the time being put in.

To understand what is driving this, I’ve analysed what has been happening in terms of output and jobs in different sectors.

Starting with growth, I’ve compared Lancashire’s top 10 sectors to UK wide GVA growth. There are some clear highlights compared to national growth in particular in professional activities, education and manufacturing.

If we’re interested in productivity - measured here as output per employment for data reasons - then we can see that the sectors listed above which have grown have also managed sustained increases in this measure of productivity.

It is very positive that the professional activities and education sectors have grown in this way - and these are the kind of service based industries that wealthier areas tend to focus on in the modern economy. In terms of education, student enrolments at the University of Lancashire are broadly flat at around 24,000 over the period so that cannot be the driver. Looking at subsectors, there have been big increases in architectural and engineering activities (GVA up 127% over 2019 to 2023) and in scientific research and development (up 97%). Would be interested in local views on what is driving this outcome.

Manufacturing has seen a big increase in GVA and a modest increase in employment. Struck by this, I looked further into the data. The biggest manufacturing subsector is ‘transport equipment’ - and in terms of employment the largest subsector is listed as ‘other transport equipment’. Regular readers may remember the same issue in Cumbria. But after further digging what turned out there to be submarines, here is ‘Manufacture of air and spacecraft and related machinery’ - so clearly relating to BAE systems and its large sites around Preston.

But we can not draw the same conclusion that defence spending is driving growth - as this subsector has not seen the large growth as we found in Cumbria. Instead it is ‘manufacture of motor vehicles’ that has taken off - increasing by 214% from £225m to £707m over the 2019 to 2023 period. Is this being driven by a spin off from British Leyland - Leyland Trucks? There is a big demand for these vehicles and a move towards electrification which could be driving this trend?

So what does the future hold for Lancashire? Two big changes to the political system are likely coming down the track.

The three upper tier local authorities of Blackpool, Blackburn with Darwen and Lancashire County Council have come together to form a Lancashire Combined Authority. At present it will be the only part of the North without a mayor as of May 2027, but it seems that the Reform leader of the County and Labour leaders of Blackpool and Blackburn are seeking to move towards a mayoral model after previous disagreements.

Lancashire will also be going through a process of ‘unitarisation’ as it moves from the old county/district model to a unitary authority model in common with other parts of the North. The government is still sifting through the responses to the recent consultation on the five options put forward by different councils, with an outcome expected soon.

The political leadership of a changed Lancashire will inherit a growing area - with high potential in some sectors and with a potential tailwind coming from defence investment if it flows into some of major employers in the area.

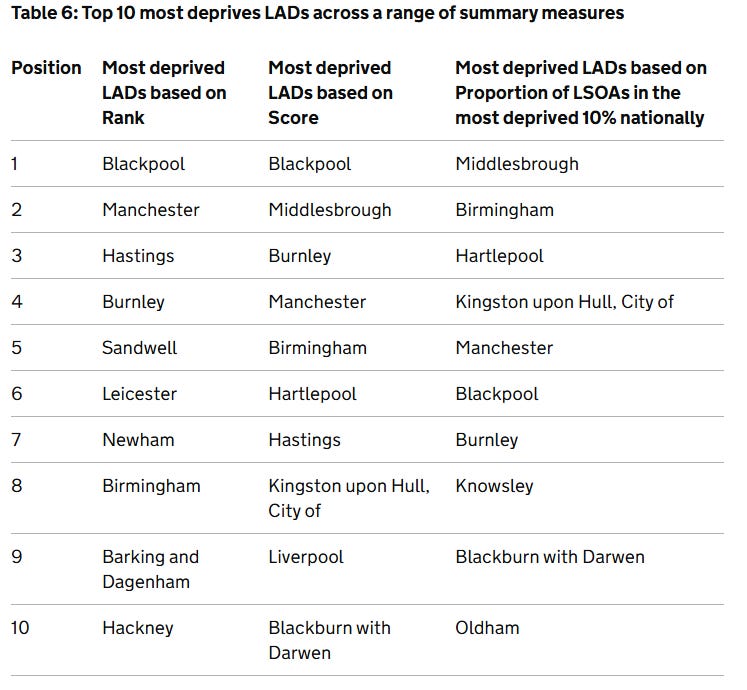

But they will also need to contend with the deprivation in parts of the area. Recent statistics showed that Blackpool, Blackburn and Burnley in particular face significant deprivation which will need addressing if growth is to translate into opportunities across Lancashire. For example, see Table 6 from the above statistics showing deprivation in Local Authority Districts (LADs).

Source: English Indices of Deprivation 2025

The data from last week’s post suggests these political reforms might be a good idea for the economy. But as the inclusion of Manchester in the deprivation table shows it might take a long time to change trajectory, even if there has been a welcome fall there according to the Centre for Cities.

We will have to see if bringing the governance of Lancashire on a par with the rest of the North will change its economic and social fortunes.

I wonder if the professional, technical and scientific sector is being driven by a strong nuclear sector? Heysham 1&2 have both recently extended their lifetimes, Westinghouse in Preston produces nuclear fuel and Lancaster University has one of the strongest nuclear science & tech research communities in the country.